Last week I shared ways we’re helping our 5 kids of varying ages and stages grow in their independence (though I regrettably forgot to mention that I wrote that post while on the road for a week and had let my big kids pack their own bags and the 9 year old packed pj’s consisting of superman boxers and a button up polo shirt. I guess he was going for half Superman/half Clark Kent. Ha! Ha!)

This week, I’m happy to share what this Kid Independence is looking like these days as it relates to chores and money. But before I jump in, I want to invite you to read a post I shared last year titled Family Chores in order to catch the spirit of how I feel about and approach chores, and also to snag a free and fantastic chore resource that has served us well. #spreadsheets!

So let’s start with my husband, Micah. I’m married to a man who has done all sorts of things- study classical guitar, serve in the Marine Corps, fly into Iraq on an Osprey, convince me to marry him within a year of meeting, go back to school again and again to develop his skills as an economist and now fiduciary for Merrill Lynch. He loves numbers, logic, pastrami sandwiches, graphs, and helping people mange their assets with courage, honesty, and integrity. So when our children began expressing interest in earning and spending money, my math-loving husband came up with a fantastic strategy…..which then sat around untouched for a long time because Project Manager Mom wasn’t ready to take on another project. Between the cooking and cleaning and laundry and schooling, serving as banker on top of all that just did not sound appealing. But as the kids’ questions continued- can I buy this? Why not? Do I have money?– and I found myself giving vague, inconsistent answers based on nothing other than my current level of patience, I knew that I was doing a disservice to the children, myself, and that fantastic plan Micah had created. It was time to implement some financial principles and practices to help the children establish financial independence. (Still cannot believe such a thought formed out of my right-brained head). A white board and a pack of dry erase markers later, and I had the beginning of our Chore Board and road map to financial independence.

Ta-da!

This board hangs in the little hallway that serves as my Command Center (more on that in next week’s post) and serves as a beautiful guide to our days as a very active-and-therefore-messy-family-of-seven.

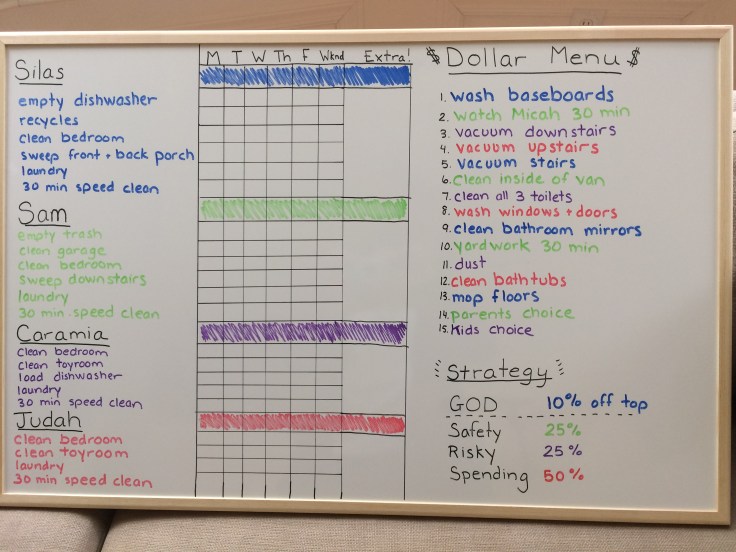

For those who love details and explanations, I will now break down the Chore Board:

Chores: Every child has been trained in their specific chores and they are to be completed as needed (dishwasher and trash, for example) or before the day ends. This usually means that the house gets restored to order immediately before or after dinner. Once a parent checks over the work, they get a check for the day.

Days of the Week: In the rare occasion that there is no laundry to fold or the bedrooms survived the day unscathed, I’ll give a ‘Pass’ for the day. Otherwise, kids are expected to complete their chores every.single.day.except for…..

Weekends: Weekend schedules aren’t very consistent, so I don’t have them complete chores on Saturday and Sunday. We all need a break from work, so my rule of thumb is as long as the house is restored to order by Sunday night, we’re good to go.

Dollar Menu: Oh my gosh, guys. The Dollar Menu! This little gem emerged into the RIGHT side of my brain no doubt as I was drawing the white board graph and man has it not disappointed! I came up with a list of chores that would actually be helpful to me and that I would be happy to pay the kids for, and then they can choose as many as they’d like throughout the week. Wanna earn enough money to buy a treat at the baseball game this week? Pick your dollar menu items, then track them on the ‘extra’ column. Only conditions: they have to confirm with me first that the specific chore will actually help me. In other words, they can’t clean the toilets the day after they were just cleaned. Surprisingly, the chore they mostly offer is babysitting Micah and it.is.awesome! Do you know how much you can get done when the baby is safely and happily contained for 30 minutes?? I’m talking a shower. Or exercise. Or reading or journaling or a phone call. It’s insane.  Strategy: Behold the beautifully logical and long-tempered vision of my husband. He took time to explain to each kid our strategy until they could teach it back to him. And then I converted it into cute little bags I found at Hobby Lobby because I wanted something cheap & lightweight that could be easily stored in our Command Center (again, more on that next week!)

Strategy: Behold the beautifully logical and long-tempered vision of my husband. He took time to explain to each kid our strategy until they could teach it back to him. And then I converted it into cute little bags I found at Hobby Lobby because I wanted something cheap & lightweight that could be easily stored in our Command Center (again, more on that next week!)

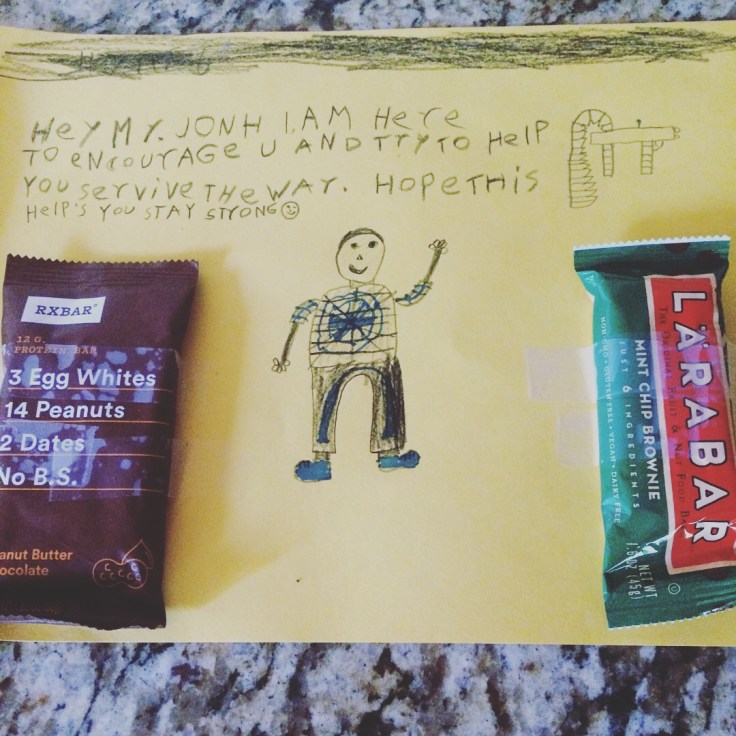

- Giving: 10% off the top goes into the “Giving” bag (labeled ‘God’ on the whiteboard) and can be used toward acts of kindness in the spirit of gratitude for God’s many gifts. For example, last month they pooled their Giving money to purchase items for a care package for a dear friend serving in Iraq. This man has been like an uncle to my children and they were so happy to purchase buffalo jerky, oatmeal packets, mints, protein bars and powdered drink mixes for their buddy Mr. Marine Corps John.

- Safety: 25% goes into their Saving bag, which is untouchable. This is their rainy day account, and just last night Silas asked if he will be able to take a percentage out of this bag when he’s 16 to purchase a car. He’s so stinking cute.

- Risky: 25% goes into their Risky bag. This is their investment money. Think Shark Tank for kids. Got an idea for a lemonade stand? Then purchase your supplies from your Risky bag. Need to print our “Firewood for Sale” signs after chopping down a tree, Sam? (true story) Then take the money from your Risky bag. The idea here is that this is money you invest with the hope of making a return but with the understanding that you might loose it. It’s a risk, and Fiduciary Daddy helps them calculate the risk.

- Spending: Last but not least, the remaining 50% goes into their Spending bag. This has been used for things like purchasing a new and long-anticipated video game for Silas, a bow and arrow that Sam researched online, a round of ice cream from the ice cream truck for all the siblings (It’s on me might’ve been uttered proudly here), nail polish for Mia….whatever makes them smile. Our one current guideline is that it cannot be an impulse purchase (ahem, Dollar Store and Target bins). We talk about what they want, set a price, and plan ahead. Otherwise, well, it’s like kids in a candy store.

- Allowance Amounts: Right now, the 9 & 8 year old boys get $5/week and the 6 and 4 year olds get $2/week. No big reasoning behind this; just picked numbers that didn’t feel ludicrous and fit into our family budget. Allowance is given out Sunday nights with much gratitude and pride. I take out enough money to last the month so I’m not constantly making last-minute trips to the ATM. Fiduciary Daddy is on hand to help with calculations and to answer questions. It’s all really adorable. Also, the middle two are now getting their $2 allowance in dimes so that (1) it looks like more money and (2) they can begin dividing it up between their strategy bags.

Well, there you have it. Our ever-evolving approach to helping our children spread their wings and fly. Or bring home the bacon. If you have a system that works for helping your kids earn & manage money, I’d love to hear about it!

We fell short raising you! This plan is amazing. I may implement it.

Thank you for sharing this!

My pleasure 🙂

So i’ve come back to this because I need this in my life now. What can you tell me about your command center and where the kids keep their money? When can they access it? Do you pay them right after they complete a dollar menu item or at the end of the week?

Great question! They get paid allowance on Sunday’s. Dollar menu items are calculated into this amount. We have a ‘bank box’ which contains their category bags. They divide up their money into each category and then it is stored away. They cannot access spending money without asking first, and to cut down on compulsive spending, I have been making it a habit to take them on a monthly trip to a store like Target or Five Below so they can buy something they have thought about for a while.